If you’re a U.S. citizen then you probably already know that today is tax filing day. We wanted to be among the first to say, lucky you. More than that, though, we’re here to help take the sting out of the occasion by offering an observation that may make these days a bit less taxing in the future.

It is often said that the U.S. tax code is designed to benefit the rich, but that is not entirely accurate. U.S. tax law is really built to favor people with assets. One is not necessarily the same as the other. Plenty of folks with high incomes manage to squander it all and, as a result, actually own very little. Others, perhaps those who have adopted our twenty-five times rule, are able to amass a considerable stash notwithstanding modest incomes. Recent changes to the tax code have been particularly friendly to this latter group of people even as they have made life more onerous for the former.

Before we get to that it’s important to first understand that the IRS does not treat all income the same. For the better part of the past 100 years the U.S. has taxed income generated by capital (interest, dividends, and capital gains) more lightly than wage income. Not only does capital income avoid the 15.3% payroll tax levied on workers and their employers, but certain types of investment income also benefits from preferentially low income tax rates.

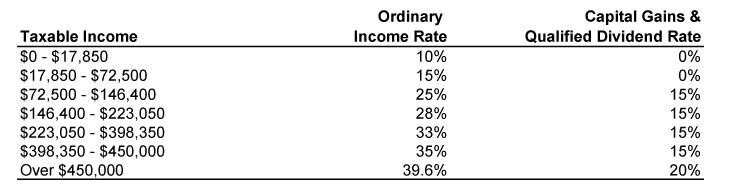

2013 Income and Capital Gains Tax Rates (married filing jointly)

Beginning in 2008 Congress reduced the tax rates applied to these privileged forms of income (specifically capital gains earned on assets held longer than one year and qualified dividends) to as low as zero for middle-income taxpayers. Married couples reporting as much as $72,500 in taxable income, and half that amount for individuals, may pay nothing at all on their capital income even though their wage income is still taxed. This January, Congress made that 0% tax bracket permanent as part of Washington’s “fiscal cliff” deal.

For an example of how this works, assume Joe and Suzy Smith are married and together will earn $80,000 from their jobs in 2013. After taking their standard deduction ($12,200) and personal exemptions ($7,600) the Smiths will report taxable income of $60,200, on which they’ll owe $8,438 in federal income taxes according to this year’s tax tables.

On $10K Gain, Uncle Sam Takes . . . $0

Now assume that during 2013 the Smiths sell stock in ABC Corp they originally bought in 2011 and realize a $10,000 long-term capital gain on the transaction. While their taxable income rises from $60,200 to $70,200 because of the gain, their income tax obligation stays the same at $8,438. Why? Because as long as they report taxable income less than $72,500, the tax rate applied to their long-term capital gain is zero.

It should be highlighted here that taxable income and actual income are two very different things. In the example above, the Smiths earned $80,000 but were only taxed on $60,200 because of their standard deduction and personal exemptions. Families with more deductions (because they have children, or own a home, or make 401(k) contributions, or for any number of other reasons) can earn far more than the Smiths – well above $100,000, even – and still be eligible for the 0% tax rate.

What’s more, the law doesn’t currently prevent the Smiths from repurchasing ABC Corp immediately after selling it. Theoretically that allows them to step up the tax basis on their stock and wipe out the tax liability on their gain forever even though they still own the shares. By opportunistically “harvesting” gains in a way that keeps the Smiths in the 0% tax bracket, they can potentially create an investment portfolio that is largely, or even entirely, tax free.

Whether the IRS will move to limit this kind of gain harvesting is anyone’s guess. They already limit loss harvesting through wash sale rules. It is possible they will extend that framework to capture realized gains as well.

But even if that happens, the zero percent tax bracket for gains is still a potentially huge tax break that can be used as part of your portfolio risk management and investment rebalancing strategy. Effectively doing so, though, first requires knowing that the zero percent tax bracket even exists. Now that you do, consult a tax professional to determine whether any of this applies to your individual circumstances.

But most of all remember to smile, it’s tax day.

Excellent post. I didn’t know about the gain harvesting. Something to think about. Would you happen to know how basis is determined when selling a mutual fund when dividends over the years have been used to buy more shares? That would appear more complicated. I’m needing a crash course on all this stuff.

LikeLike

Hi Jennifer,

There are multiple methods for calculating basis (average cost, First In First Out, and specific identification) that will all yield different results. Your mutual fund may have already asked you to choose a method (or may require you to choose one when you go to sell). Fund companies are now required to report your basis to the IRS when you sell shares so they should also be able to help you calculate it for your own purposes.

Here’s a link to a Bogleheads article discussing the different methods. http://www.bogleheads.org/wiki/Cost_basis_methods

Cheers,

Brian

LikeLike

Great. Thanks so much Brian.

LikeLike

Was oblivious to these recent changes. Wow, 0% on $72.5K is great news.

Thanks!!!

LikeLike